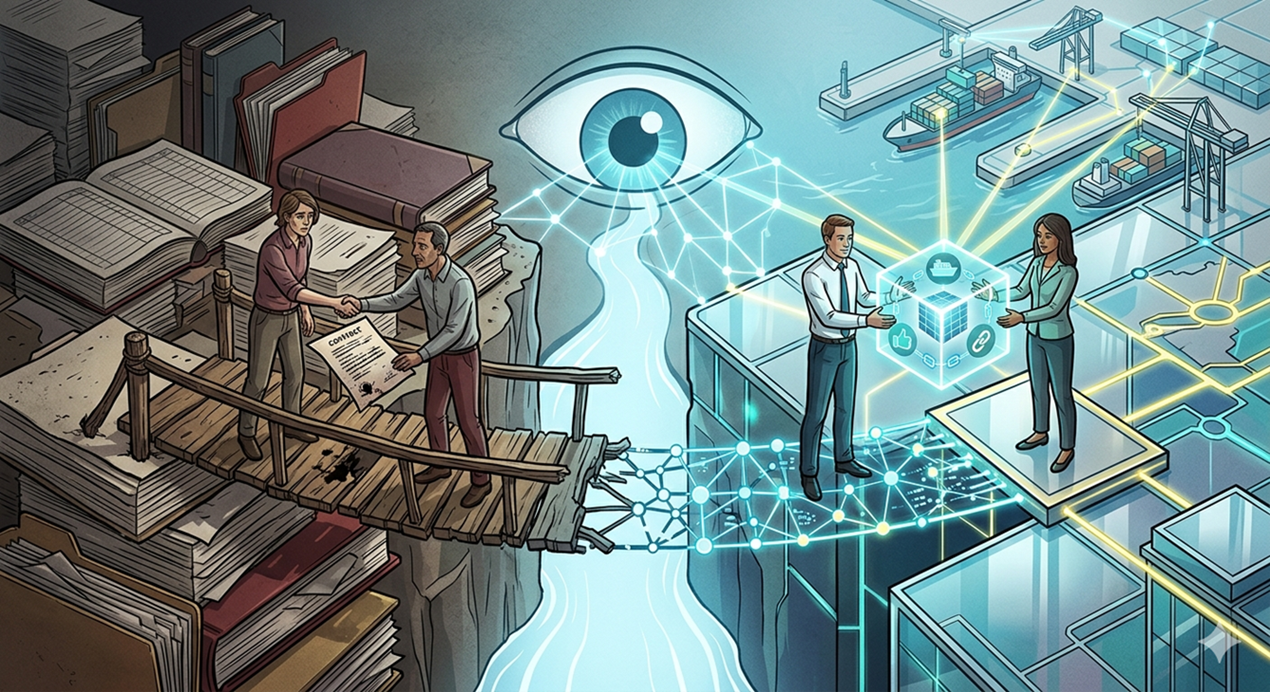

For generations, global trade has relied on a simple ritual: documents stamped, signed and shipped across borders. That ritual is now being quietly dismantled.

A container leaves Chittagong bound for Rotterdam.

The goods move in days.

The documents take weeks.

This mismatch — between the speed of logistics and the slowness of paperwork — has long defined trade finance. It is also the reason why the industry now finds itself under pressure to change.

From electronic bills of lading to blockchain platforms and artificial intelligence, the machinery of global trade is undergoing a gradual but profound transformation. The question is no longer whether trade finance will go digital, but how — and at what cost.

The Paper Paradox

Trade finance was built on paper for a reason.

Physical documents created:

- Proof of shipment

- Evidence of ownership

- Legal enforceability

- A chain of trust between unknown parties

Under frameworks shaped by the International Chamber of Commerce, particularly the rules of UCP 600, banks learned to rely on documents rather than goods.

This model worked. It still does.

But it comes at a cost.

A single transaction may require dozens of documents, each manually checked, physically transported and repeatedly verified. Errors are common. Delays are routine. Fraud, though limited, is not unknown.

In an era of real-time communication, trade finance has remained stubbornly analogue.

The Push Toward Digital

The shift away from paper is not driven by theory but by necessity.

Global supply chains are faster, more complex and more data-driven than ever before. Businesses expect speed. Banks demand efficiency. Regulators require transparency.

Digital documentation promises all three.

Electronic Bills of Lading

Perhaps the most significant innovation is the electronic bill of lading (eBL).

Traditionally, this document represents ownership of goods and must be physically transferred. Its digital equivalent allows ownership to be transferred instantly — removing one of the biggest bottlenecks in trade.

The implications are significant:

- Faster release of goods

- Reduced risk of document loss

- Lower administrative costs

Yet adoption remains uneven, held back by legal and operational concerns.

Digital Letters of Credit

Banks are also experimenting with fully digital documentary credits.

In theory, this allows:

- Instant issuance and amendment

- Real-time document submission

- Automated compliance checks

In practice, the transition is gradual. Many transactions still rely on hybrid systems — part digital, part paper.

Blockchain: Promise and Reality

No discussion of digital trade finance is complete without blockchain.

Often described as a “trust machine”, blockchain offers a shared, tamper-resistant record of transactions accessible to all participants.

Its appeal is clear:

- A single version of truth

- Reduced duplication

- Greater transparency

- Lower fraud risk

In a system where multiple parties verify the same documents, blockchain offers the possibility of eliminating redundancy.

But reality is more complicated.

The Barriers

- Lack of standardisation across platforms

- Regulatory uncertainty

- Integration challenges with existing banking systems

- Reluctance among participants to change established processes

For now, blockchain remains promising but not dominant — a technology searching for universal adoption.

The Quiet Rise of Artificial Intelligence

While blockchain attracts headlines, artificial intelligence is already reshaping trade finance behind the scenes.

AI systems can:

- Detect inconsistencies in documents

- Identify unusual transaction patterns

- Screen for sanctions and compliance risks

- Reduce manual workload

For document examiners, this means fewer routine checks and more focus on judgment.

Yet AI has limits.

It can process data quickly, but it cannot fully interpret context. It can flag anomalies, but it cannot replace professional responsibility.

The human element remains central.

Data: The New Currency of Trade

Perhaps the most transformative aspect of digital trade finance is not technology itself, but the data it generates.

Paper documents contain information.

Digital systems create intelligence.

With structured data, banks can:

- Analyse trade flows

- Assess client behaviour

- Predict risk patterns

- Improve pricing models

This shift changes the nature of trade finance.

It moves from a document-processing function to a data-driven business.

New Risks in a Digital World

Digitalisation solves some problems — and creates others.

The most immediate concern is cybersecurity.

In a paper-based system, fraud involves forged documents.

In a digital system, it involves compromised platforms.

Banks must now protect:

- Sensitive trade data

- Financial transactions

- Client identities

A cyber breach can have consequences far beyond a single transaction, potentially disrupting entire supply chains.

Trust, once anchored in paper, must now be secured through technology.

The Legal Question

Technology alone cannot transform trade finance. Law must follow.

For digital documents to replace paper, they must be:

- Legally recognised

- Enforceable across jurisdictions

- Accepted by courts

Progress is being made, but unevenly.

Some countries have embraced electronic trade documentation. Others remain cautious. The result is a fragmented landscape where digital adoption depends as much on regulation as on technology.

Emerging Markets: Opportunity and Risk

For countries like Bangladesh, the digital transformation of trade finance presents both promise and challenge.

The Opportunity

- Faster export processing

- Lower transaction costs

- Greater access to global markets

The Challenge

- Limited digital infrastructure

- Need for regulatory reform

- Skills gap in technology adoption

The risk is not that digital trade will fail — but that its benefits will be unevenly distributed.

The Changing Role of Banks

As trade finance evolves, so too does the role of banks.

They are no longer just intermediaries verifying documents. Increasingly, they are:

- Platform operators

- Data managers

- Risk analysts

- Technology integrators

This shift requires new capabilities — and a new mindset.

For professionals, including CDCS candidates, the implication is clear:

Understanding rules is no longer enough.

Understanding systems is essential.

A System in Transition

Despite rapid innovation, trade finance will not become fully digital overnight.

The industry is cautious for good reason:

- Transactions involve high values

- Legal certainty is critical

- Trust must be preserved

As a result, the transition is gradual — a coexistence of old and new.

Paper and digital systems operate side by side.

Manual checks complement automated processes.

Tradition and innovation move together.

Conclusion: Reinventing Trust

Trade finance has always been about trust.

In the past, that trust was built on paper — documents stamped, signed and verified.

Today, it is being rebuilt through code, data and digital platforms.

The tools are changing.

The risks are evolving.

The opportunities are expanding.

But the core question remains the same:

How do strangers, separated by distance and jurisdiction, trust each other enough to trade?

The answer, increasingly, will not be found in paper files or courier envelopes.

It will be found in systems — digital, interconnected and still being defined.

For those preparing to enter the profession, the message is clear:

The future of trade finance is not paperless.

It is trust — reimagined.

CDCS Master Series – examining not only how trade finance works today, but how it is being reshaped for tomorrow.